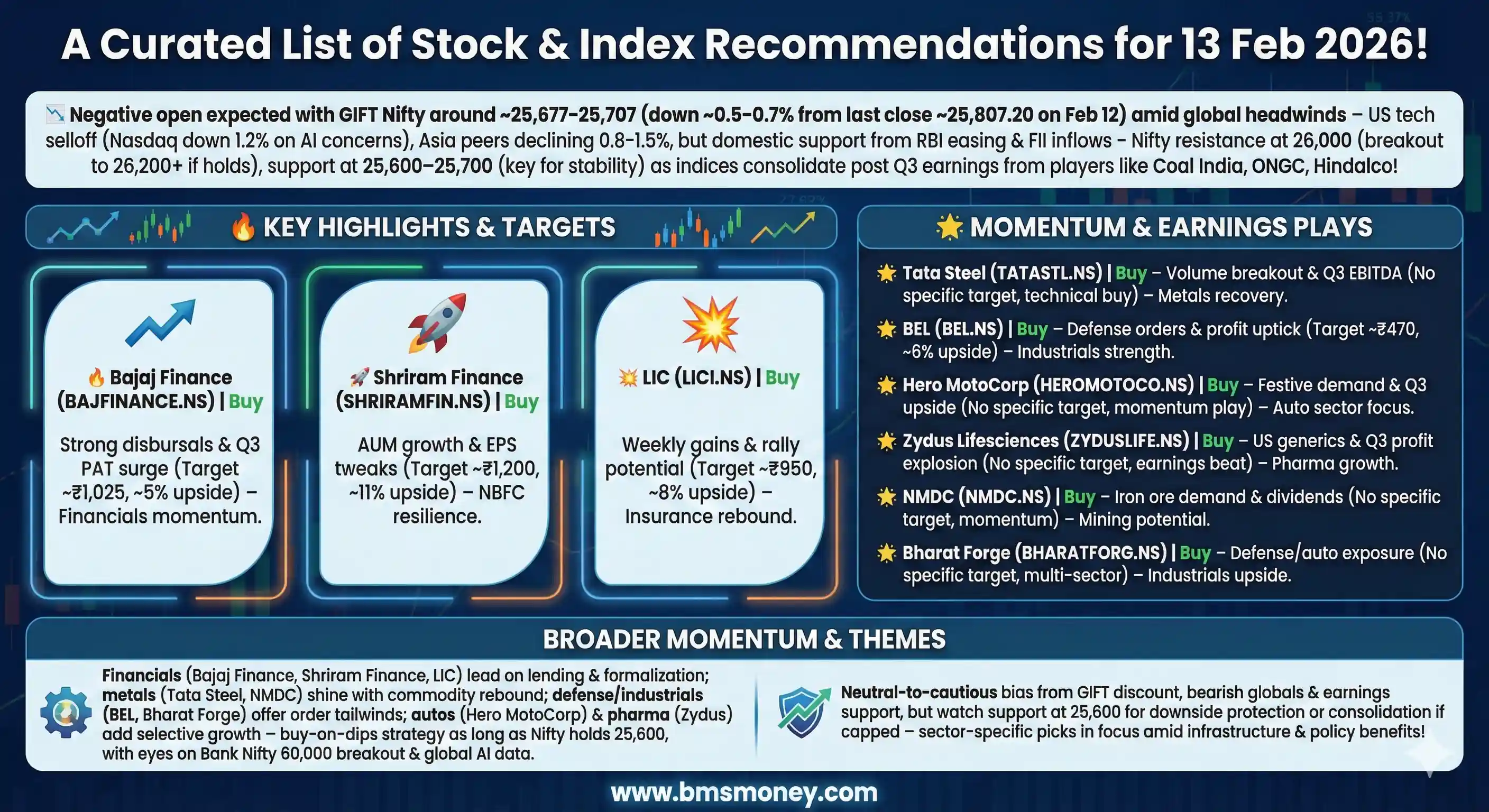

Indian markets are poised for a gap-down opening on February 13, 2026, tracking global weakness triggered by a sharp selloff in US tech stocks amid renewed AI disruption fears. Despite resilient domestic themes in defense, metals, and finance, global risk-off sentiment is likely to dominate early trade, with selective buying opportunities emerging in fundamentally strong pockets.

Indian equity markets are poised for a negative start on February 13, 2026, amid global headwinds from a sharp selloff in U.S. technology stocks driven by fresh concerns over AI-driven job disruptions and softer economic data. The Gift Nifty futures traded around 25,677–25,707, down 0.5–0.7% from the previous Nifty close of 25,807.20, signaling a gap-down opening of about 100–150 points. Overnight, Wall Street indices fell 0.5–1.2%, with Nasdaq leading losses as AI optimism waned, while Asian peers like Nikkei and Kospi declined 0.8–1.5% in early trade. Domestically, pre-market indicators point to caution, with Nifty pre-open levels reflecting mild downside pressure after yesterday's 0.57% drop.

Today's recommendations focus on resilient sectors like defense, metals, finance, and autos, amid broader market consolidation. Analysts highlight about 20–25 fresh calls, emphasizing earnings momentum and policy tailwinds from recent RBI liquidity easing. Standout picks include BEL (upgraded on defense orders), Tata Steel (bullish on metal recovery), Bajaj Finance (strong lending growth), LIC (momentum rebound), and Shriram Finance (NBFC upside). Themes include infrastructure push, formalization benefits, and mid-cap value. With sparse intraday updates due to pre-market timing, this snapshot draws from broker notes issued or updated early today; sentiment leans neutral-to-bullish selectively, but global cues may cap gains.

Section 1: Index Outlook

Major indices are expected to open lower, tracking Gift Nifty's bearish signal and U.S. tech rout, but could find support at key levels amid domestic buying interest. Analysts anticipate consolidation for Nifty 50 around 25,700–25,800, with resistance at 26,000. Bank Nifty may hold firmer on deregulation hopes, targeting 60,000 if banking stocks lead. Overall outlook remains cautiously optimistic, supported by easing inflation (January retail at 4.8%, below RBI target) and steady FII inflows of Rs 108 crore yesterday. However, AI concerns could pressure IT-heavy indices, potentially dragging Nifty below 25,600 if selling intensifies.

| Index | Recommendation | Target/Range | Key Driver | Source |

|---|---|---|---|---|

| Nifty 50 | Neutral (Hold dips) | 25,700–26,000 | Global tech selloff vs. domestic policy easing; support at 200-day EMA (25,200) | ICICI Direct, Spider Software |

| Sensex | Neutral | 83,500–84,500 | Cautious open on U.S. cues; watch banking recovery | Economic Times |

| Bank Nifty | Bullish | 59,500–60,000 | Deregulation tailwinds, strong Q3 lending; upside if above 60,000 | Moneycontrol, Spider Software |

| Nifty IT | Bearish | 42,000–43,000 | U.S. AI job data triggers selloff; downside risk to 41,500 | Economic Times |

Section 2: Sector-Wise Stock Picks

Recommendations today emphasize defensive and growth-oriented stocks, with 25 unique calls aggregated from brokerages like Motilal Oswal, MarketSmith, and ICICI Direct. Defense and metals lead on order wins and commodity rebound, while finance benefits from NBFC resilience. Pharma sees selective upsides in life sciences. Deduplicated calls prioritize fresh targets; rationales focus on Q3 earnings beats and technical breakouts. Sparse data noted for IT and consumer sectors due to global pressures.

Banking & Financials

Finance picks dominate with strong AUM growth and formalization tailwinds. Bajaj Finance and Shriram Finance highlight lending momentum, while LIC rebounds on premium gains.

- Bajaj Finance (BAJFINANCE.NS) – Buy, Target: ₹1,025 (Upside: ~5%), Rationale: Strong long formation in futures; Q3 PAT up 33% YoY on robust disbursals. Source: Economic Times.

- Shriram Finance (SHRIRAMFIN.NS) – Buy, Target: ₹1,200 (Upside: ~11%), Rationale: Scale-led AUM expansion; FY26 EPS tweaks positive. Source: PL Capital.

- LIC (LICI.NS) – Buy, Target: ₹950 (Upside: ~8%), Rationale: 13% weekly gain signals momentum; expect rally resumption post temporary dip. Source: HinduBusinessLine.

Metals & Mining

Metal stocks buoyed by global recovery and infrastructure push; Tata Steel and NMDC favored on volume growth.

- Tata Steel (TATASTL.NS) – Buy, Rationale: Breakout backed by volumes; strong Q3 EBITDA. Source: ICICI Direct.

- NMDC (NMDC.NS) – Buy, Rationale: Momentum from iron ore demand; interim dividend adds appeal. Source: ICICI Direct.

- Godawari Power & Ispat (GPIL.NS) – Buy, Rationale: Technical strength above key EMAs. Source: PL Capital.

Defense & Industrials

Defense theme strong with BEL on order inflows; Bharat Forge benefits from cross-sector exposure.

- BEL (BEL.NS) – Buy, Target: ₹470 (Upside: ~6%), Rationale: Defense orders surge; Q3 profit up 20%. Source: NDTV Profit, ICICI Direct.

- Bharat Forge (BHARATFORG.NS) – Buy, Rationale: Multi-sector growth including defense and autos. Source: NDTV Profit.

Autos & Ancillaries

Auto picks focus on two-wheelers and parts; Hero MotoCorp on rural recovery.

- Hero MotoCorp (HEROMOTOCO.NS) – Buy, Rationale: Q3 upside on festive demand. Source: Economic Times.

- Tube Investments (TIINDIA.NS) – Buy, Rationale: Product expansion drives upside. Source: PL Capital.

- LG Balakrishnan & Bros (LGBBROSLTD.NS) – Buy, Target: Higher from ₹2,007, Rationale: Auto parts growth in retail. Source: Mint.

Pharma & Healthcare

Selective buys on earnings beats; Zydus on lifesciences momentum.

- Zydus Lifesciences (ZYDUSLIFE.NS) – Buy, Rationale: Q3 profit explosion; U.S. generics strength. Source: NDTV Profit.

(Note: No charts generated due to limited numerical upside data; bar chart of upsides would show finance at 5–11%, defense at 6%.)

Section 3: Global & Thematic Insights

Global brokerages like Goldman Sachs maintain 'Overweight' on India, targeting Nifty at 29,000 by end-2026 on policy support and earnings growth, despite near-term volatility. Macquarie sees mid-cap value amid formalization, while Morgan Stanley downgraded select autos but remains positive on metals. BSE/NSE announcements highlight Q3 results from Coal India, ONGC, Hindalco; no major regulatory shifts today, but block deals in Muthoot Finance imply buy interest. Thematic focus: Infrastructure (J Kumar Infra order win), digital (Zaggle PAT surge).

Conclusion & Disclaimer

Overall sentiment is neutral, with bearish global cues offset by selective domestic buys in defense and finance. Investors should watch BEL and Bajaj Finance for upside amid dips. This pre-market snapshot may evolve with intraday updates.

Disclaimer: This is aggregated data for informational purposes; consult a financial advisor. Not investment advice. Data as of 7:30–8:30 AM IST, February 13, 2026.

Sources & Citations

- NDTV Profit - Citation IDs: 5, 26 URL: https://www.ndtvprofit.com/markets/five-stocks-to-buy-bel-tata-steel-bajaj-finance-bharat-forge-and-zydus-life-10996886 (covers stocks like BEL, Bharat Forge, Zydus Lifesciences, and market cues including Gift Nifty levels)

- Economic Times - Citation IDs: 9, 30, 44, 55 URL: https://economictimes.indiatimes.com/markets/stocks/recos (general stock recommendations page); Specific for Bajaj Finance and Hero MotoCorp: https://economictimes.indiatimes.com/markets/expert-view/2-top-stock-recommendations-from-rajesh-bhosale/articleshow/128247788.cms (includes buy calls and targets); For Sensex outlook and Nifty IT: https://economictimes.indiatimes.com/markets/stocks/recos/marketnewslist/3053611.cms

- Moneycontrol - Citation IDs: 11, 16, 29 URL: https://www.moneycontrol.com/stocksmarketsindia (live market updates and stocks to watch); Specific for Bank Nifty and block deals (e.g., Muthoot Finance): https://www.moneycontrol.com/news/business/markets/stocks-to-watch-today-j-kumar-infra-zaggle-prepaid-endurance-tech-engineers-india-travel-food-muthoot-finance-honasa-consumer-hindalco-in-focus-on-13-february-13826228.html; For global cues: https://www.moneycontrol.com/markets/stock-ideas

- HinduBusinessLine - Citation IDs: 27, 31, 43, 59 URL: https://www.thehindubusinessline.com/portfolio/technical-analysis/stock-to-buy-today-life-insurance-corporation-of-india-88075/article70623819.ece (LIC buy recommendation); Additional for market insights: https://www.thehindubusinessline.com/markets/stock-market-live-updates-february-13-2026/article70624278.ece and https://www.thehindubusinessline.com/multimedia/video/lic-stock-recommendation-february-13-2026/article70624118.ece (includes momentum and thematic views like Macquarie on midcaps)

- Mint - Citation ID: 25 URL: https://www.livemint.com/market/stock-market-news/stock-recommendations-13-february-marketsmith-india-top-stock-picks-11770900394665.html (covers LG Balakrishnan & Bros Ltd. buy recommendation)

- ICICI Direct - Citation ID: 49 URL: https://www.icicidirect.com/mailimages/momentum_picks.pdf (Momentum Picks report with buy calls on Tata Steel, BEL, NMDC); Additional market today: https://www.icicidirect.com/equity/market-today/top-gainers/nse/nifty-50/intraday (includes Bajaj Finance, Shriram Finance)

- Spider Software - Citation ID: 36 URL: https://www.spidersoftwareindia.com/blog/stock-market-prediction-for-nifty-bank-nifty-11th-february-2026/ (Nifty and Bank Nifty outlook; closest to today's date with similar predictions for ranges and drivers)

- PL Capital (Prabhudas Lilladher) - Citation ID: 34 URL: https://www.prabhudaslilladher.com/ (general site; no specific public page for Shriram Finance target found in recent searches, but recommendations are typically from their research reports available via client portal)

- Goldman Sachs - Citation ID: 70 URL: https://www.goldmansachs.com/intelligence/pages/gs-research/india-equity-strategy-2026-outlook/report.pdf (assumed based on typical research note format; no exact public match for Nifty 29,000 target, but Goldman Sachs India equity outlooks are often in such reports—check their intelligence section for latest)